Phase-out of the CMS IPO list: What it means for site-of-care shifts, volumes, and revenue mix

Feb 3rd, 2026

A long-standing barrier to outpatient surgical care is coming down that will reshape where and how procedures are performed, creating substantial opportunities for surgery centers.

For years, the CMS Inpatient-Only (IPO) list kept complex surgeries anchored in hospitals. As procedures became safer and recovery times shortened, its role became increasingly debated, yet reimbursement rules kept many cases firmly inpatient.

That constraint is now being lifted.

CMS is finalizing its plan to phase out the IPO list over a three-year period starting in 2026. The policy change doesn’t force providers to move cases out of the hospital. But it removes one of the last structural barriers that kept high-value procedures concentrated there. The downstream effects—on volume, revenue mix, and competition—are expected to be significant.

What is the CMS Inpatient-Only (IPO) list?

The IPO list defines which procedures Medicare will only reimburse when performed in an inpatient hospital setting. Historically, procedures landed on the list because they were considered too complex or risky for outpatient settings and required hospital-level care.

Over time, clinical practice has changed. Advances in anesthesia, minimally invasive techniques, and post-acute care made many procedures feasible in outpatient environments. Still, the IPO list limited where Medicare dollars could follow.

For hospitals, that restriction matters. It helps preserve inpatient surgical volume for major orthopedic surgeries, certain cardiac procedures, and other complex surgeries, and protects revenue tied to service lines that often carry strong margins.

What changes are starting in 2026?

CMS started phasing out the IPO list by removing 285 procedures, mostly musculoskeletal, from inpatient-only restrictions in 2026. These procedures can now be reimbursed in hospital outpatient departments (HOPDs) and, where appropriate, ambulatory surgery centers (ASCs), creating a potential multi-billion-dollar opportunity for ASCs.

The shift doesn’t eliminate clinical judgment. Providers retain discretion to admit patients when medically necessary. What changes is the financial flexibility. When reimbursement no longer dictates site of care, operational efficiency and economics start to carry more weight in decision-making.

That flexibility comes at a time when hospitals are already under pressure from rising expenses and shifting healthcare policies that could further strain hospital margins.

How IPO phase-out accelerates site-of-care shifts

In recent years, CMS has gradually removed individual procedures from the IPO list, nudging more care to outpatient settings and ASCs. The upcoming full IPO phase-out will speed up this migration.

Past IPO removals, including hip and knee replacements, show that procedure migration can be rapid once inpatient restrictions lift. While the pace will vary by procedure (and not all procedures will migrate), historical patterns suggest hospitals should prepare for substantial volume shifts within a few years.

The charts below illustrate how site-of-care trends have evolved over time.

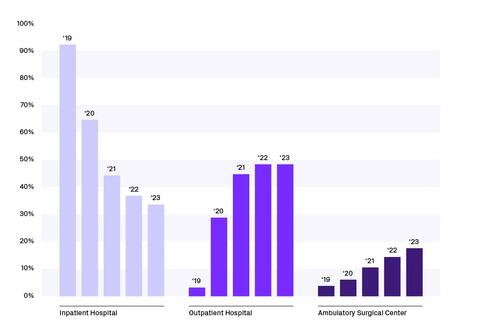

Share of inpatient, outpatient, and ASC hip surgeries, 2019 – 2023

Fig. 1 – Share of hospital inpatient, hospital outpatient, and ambulatory surgery center (ASC) hip surgeries from 2019 – 2023 based on Definitive Healthcare data.

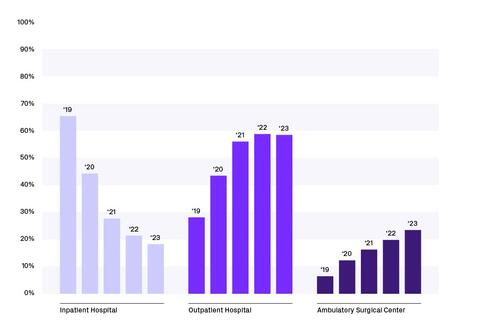

Share of inpatient, outpatient, and ASC knee surgeries, 2019 – 2023

Fig. 2 – Share of hospital inpatient, hospital outpatient, and ambulatory surgery center (ASC) knee surgeries from 2019 – 2023 based on Definitive Healthcare data.

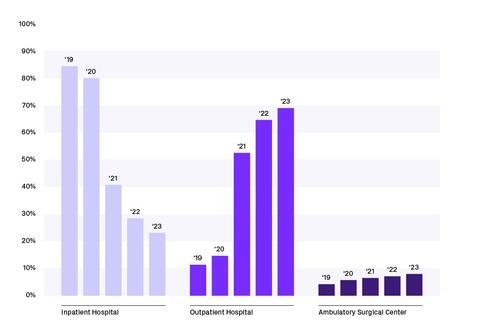

Share of inpatient, outpatient, and ASC shoulder surgeries, 2019 – 2023

Fig. 3 – Share of hospital inpatient, hospital outpatient, and ambulatory surgery center (ASC) shoulder surgeries from 2019 – 2023 based on Definitive Healthcare data.

Many of the procedures affected are high-margin cases that hospitals have relied on to offset lower-paying services. Once those procedures are no longer locked to inpatient reimbursement, the incentive to move them grows quickly. Outpatient settings typically offer lower overhead, greater convenience, and faster turnover.

HOPDs will capture some of this volume. ASCs, which are typically lower-cost, will capture a lot of it. It’s worth noting that commercial payors and Medicare Advantage plans have long used the IPO list as a guide for coverage and site-of-care rules. As the list disappears, these payors will likely speed up their own moves toward outpatient settings, pushing procedure migration beyond traditional Medicare.

Impact on procedure volumes and revenue mix

The most immediate impact of the IPO phase-out is not lost volume, but redistributed volume, which creates exposure for service lines that previously subsidized other hospital operations. Inpatient surgeries may fall as total surgical volume stays flat or even grows. However, inpatient cases generate higher reimbursement per procedure, and outpatient growth is unlikely to replace that revenue dollar-for-dollar. Moreover, as lower-risk patients move to ASCs, remaining inpatients will be more medically complex, driving up post-acute costs.

What this means for hospitals, ASCs, and medtech

Hospitals face the most immediate exposure. The key question isn’t whether volume will shift, but which hospitals and service lines are most vulnerable and how much revenue is at stake. At-risk organizations that wait for inpatient volumes to decline before responding will find themselves reacting too late.

ASCs are positioned for growth, but not automatically. The biggest gains will go to centers that understand which procedures are moving, which surgeons are driving that shift, and how capacity needs to evolve depending on the market. The opportunity won’t look the same in every market.

Medtech companies sit in the middle of these changes. As surgeries move out of hospitals, purchasing behavior can change with it. Hospital-focused selling strategies may not translate cleanly to ASCs, and account targeting based on historical hospital volume can miss where surgeries are actually happening. Sales teams, in particular, need a clear picture of where procedures are going across geographies, care sites, and surgeons.

Using claims data to anticipate and respond

Claims data and market intelligence make it possible to see procedure migration across different care settings. The right data can help spot which surgeons and ASCs are gaining share, where inpatient exposure is highest, and how revenue mix is likely to change under different scenarios.

Organizations can use these insights to quantify revenue at risk, forecast future volume, and align commercial and operational strategies with real-world utilization, not assumptions.

Looking ahead

The IPO list phase-out is part of a broader shift toward a more competitive surgical landscape. Providers and manufacturers that leverage data to understand where care is actually shifting will be positioned to adapt before the numbers show up on a financial statement.

Definitive Healthcare helps you see where care is really happening across hospitals, ASCs, and other healthcare settings, so you can grow where the market is moving. Sign up for a demo.

You might also be interested in...